- Strategic Structuring

- Risk Mitigation

Capital Markets

- Digital Engagement

- Market Visibility

Public Perception

- Shareholders Services

- EDGAR Filings

On May 20, 2026, Space Exploration Technologies Corp. publicly filed a Form S-1 with the SEC (accession no. 0001628280-26-036936). The company applied to list on Nasdaq and Nasdaq Texas under the ticker SPCX. Reported terms point to a valuation target of approximately $1.75 trillion and a capital raise of up to $75 billion, which would make this the largest IPO on record. The roadshow is expected to start in early June, with pricing and listing targeted for mid-June. [SEC] [Reuters]

The most important framing point is that SPCX will not trade as a pure-play rocket business. The S-1 financials fold in xAI (which itself absorbed the X platform in March 2025) following the February 2026 xAI/SpaceX merger. Because the entities were under common control, results have been retroactively combined and restated. Standalone SpaceX generated roughly $15 to $16 billion of 2025 revenue, but the combined entity reports $18.67 billion.

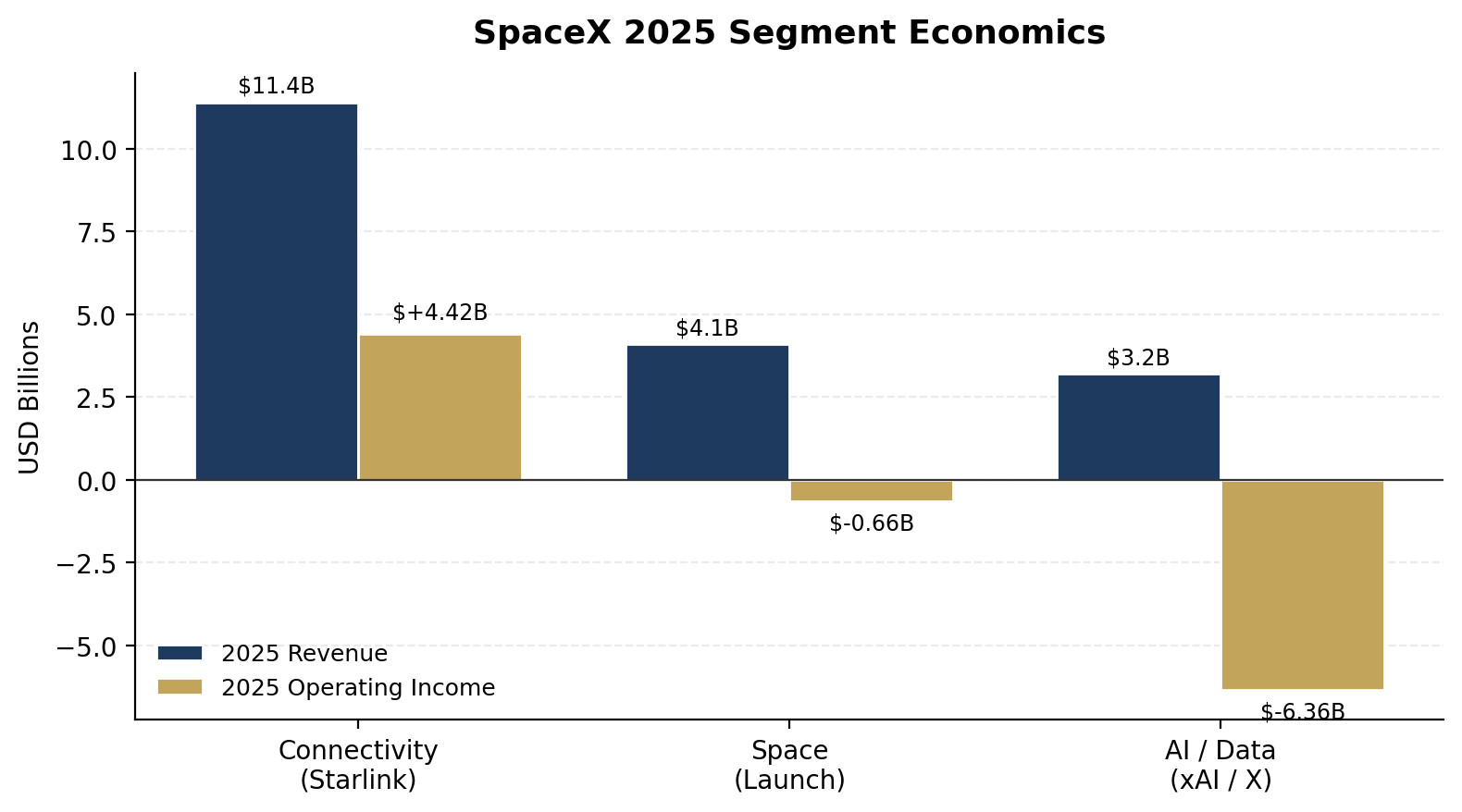

This is the original SpaceX business: Falcon 9 and Falcon Heavy, Dragon, and Starship development. Falcon 9 has logged 620+ orbital launches with a 99%+ success rate and at least one booster on 34 reflights. SpaceX is currently responsible for more than 80% of mass to orbit globally. Starship is the strategic bet. 2025 segment revenue was $4.09 billion with an operating loss of $657 million driven by roughly $3 billion of Starship R&D in 2025. Adjusted segment EBITDA was positive $653 million. Federal contracts contribute approximately one-fifth of total company revenue.

Connectivity is overwhelmingly Starlink, with 10.3 million subscribers as of Q1 2026 (up from 5.0 million a year earlier). The segment generated $11.39 billion of 2025 revenue and $4.42 billion of operating income — a 39% operating margin. In Q1 2026 it generated $3.26 billion of revenue and $1.19 billion of operating profit. ARPU has compressed from $81 at year-end 2025 to $66 in Q1 2026 (lower-priced geographies and mobile partnerships), but absolute growth is still 50% to 57% year over year. Terminal manufacturing costs fell roughly 59% in 2025. [Fool]

This segment is the result of the xAI merger. It includes xAI's model business, X platform revenue, and the COLOSSUS and COLOSSUS II data centers in Memphis. In 2025 it generated $3.20 billion of revenue and an operating loss of $6.36 billion. In Q1 2026 alone it lost $2.47 billion on $818 million of revenue and absorbed 76% of total Q1 capex. This segment is the reason consolidated SpaceX swung from an estimated $791 million net profit standalone to a $4.94 billion combined net loss after restatement. [Axios]

The headline disclosure here is the Anthropic compute deal: $1.25 billion per month through May 2029, with a 90-day mutual termination right and discounted billing during the May/June 2026 ramp. If it runs full term, that is more than $40 billion of contracted revenue. Two cautions: the 90-day exit is unusually short for a data-center anchor contract, and SpaceX consolidates xAI, which competes directly with Anthropic. [Axios]

Figure 1. 2025 segment revenue and operating income.

Consolidated 2025 highlights: revenue $18.67B (combined; ~$15-16B standalone), adjusted EBITDA $6.58B, net loss $4.94B (vs. $791M standalone net profit in 2024), capex $20.74B with another $10.1B in Q1 2026, cash ~$24.8B, and a $20 billion SpaceX Bridge Loan outstanding as of April 30, 2026 that may need to be refinanced from IPO proceeds. [Reuters]

A public S-1 at this stage is a complete substantive disclosure for the business but a deliberately incomplete document on offering economics. The May 20 filing follows that pattern. For directors and IR teams, the blanks below are the items to track in the next amendment.

The S-1 states net proceeds will be used "to fund our growth strategy," with specific reference to expanding AI compute infrastructure. The dollar allocation between AI capex, launch and connectivity expansion, working capital, and bridge-loan repayment is not pinned down. Three offering-economics fields are also still blank:

• Initial public offering price per share — the dilution section shows the price as a blank input.

• Number of shares offered — the Gibson Dunn legal opinion exhibit refers to "up to [blank] shares."

• Authorized capital structure — the form of restated certificate of formation has blank totals overall and by class.

Reported targets ($1.75T-$2T valuation; up to $75B raised) would imply roughly 4.3% float at the low end. Until those blanks fill in, they remain deal-talk numbers, not prospectus terms.

The S-1 introduces a staged lockup that departs from the standard 180-day post-IPO restriction. Subject to company and stock-price performance, certain pre-IPO holders may be eligible to sell as early as the first quarterly earnings release after listing, with additional staged releases over the following months. Musk and certain other significant holders have agreed to a 366-day restriction. The total shares in the staged lockup, and the identity of the early-release holders, are not disclosed; key figures are redacted. A staged release smooths supply versus a single cliff, but selling pressure can emerge as early as the first earnings cycle. [Reuters]

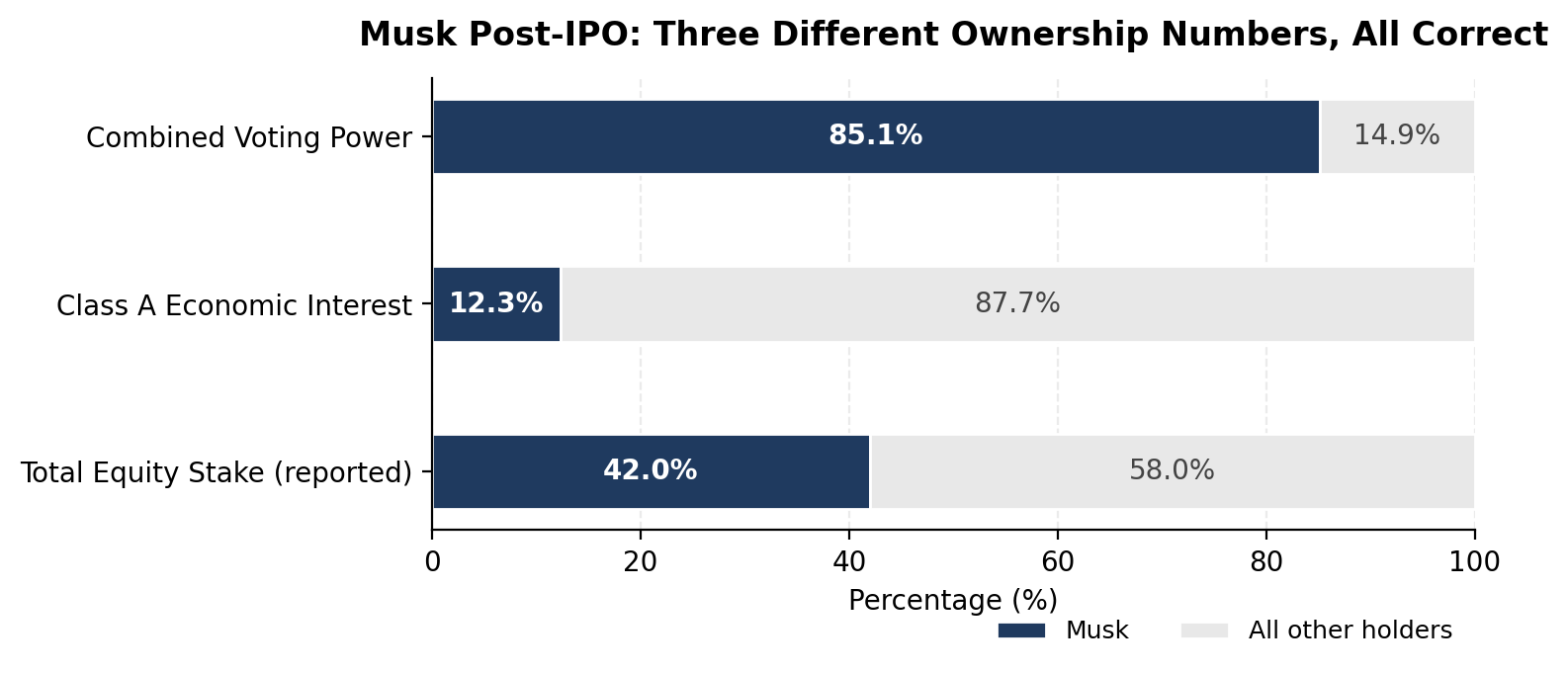

SpaceX has a three-class structure: Class A (one vote), Class B (ten votes), Class C (no votes except where required). Class B holders, voting separately, elect 51% of the board. Post-IPO, Musk retains 85.1% of combined voting power, 12.3% of the Class A economic interest, and approximately 42% of total equity. Three different concepts, three different numbers, all correct. [Reuters] [Fortune]

Figure 2. Three correct ownership measurements for Musk after the IPO.

Two compounding governance features: SpaceX is electing controlled-company status under Nasdaq rules (no majority-independent-board requirement; non-independent comp and nominating committees permitted; audit committee still independent under SEC rules), and Musk cannot be removed from the board, CEO, or chair role except by Class B vote, which he controls. CalPERS and the New York City and State controllers wrote to management in mid-May calling the package among the most management-favorable governance structures ever proposed for a U.S. listing. The bylaws and form of indemnification agreement are also still filed as forms with blank effective dates. [Fortune]

Elon Musk — Founder, CEO, CTO, Chair (since May 2002). Concentrates operating credibility (the dominant commercial launch provider, an $11B-revenue Starlink) and key-person risk in one person. The governance package structurally insulates his role from public shareholder action. The xAI consolidation makes his other ventures more directly relevant to SPCX shareholders than is typical, and the S-1 discloses ongoing Grok image-generation litigation. [Reuters]

Gwynne Shotwell — President and COO (joined 2002, President since 2008). Northwestern BS Mechanical Engineering and MS Applied Mathematics, both with honors; ten-plus years at The Aerospace Corporation before SpaceX. Built the Falcon manifest to ~170 launches and more than $20 billion of contracted business; sits on the SpaceX board; estimated to hold ~0.3% of equity. The operating counterweight to Musk's product ambitions, and the executive most responsible for converting them into delivered launches and customer contracts.

Bret Johnsen — Chief Financial Officer (since 2011). USC accounting (BS), San Diego State finance (MS), CPA; prior CFO at Mindspeed Technologies and senior finance at Broadcom. Sits on the board; reported to hold approximately 9.6 million post-split shares. Will own the post-IPO communications cadence and the bridge from private-company narrative to quarterly disclosure discipline. Signed the December 2025 tender-offer letter that anchored the most recent secondary at $421 per share / $800B valuation.

Antonio Gracias — director and founder/CEO of Valor Equity Partners. Valor-affiliated entities hold >500 million post-split shares (~7.3% of Class A pre-IPO), by far the largest disclosed non-Musk position. Voting alignment with founder management is well established. [Business Insider]

Per CNN's review of the May 20 filing, the rest of the board comprises Luke Nosek (Gigafund; earlier Founders Fund), Steve Jurvetson (Future Ventures; earlier DFJ), Randy Glein (DFJ Growth), Ira Ehrenpreis (DBL Partners; also on Tesla's board — worth noting for interlocking-director purposes), and Donald Harrison (Google executive, reflecting Alphabet's earlier investment). Other holders commonly mentioned in cap-table coverage include Founders Fund, Sequoia, Fidelity, D1 Capital, Thrive Capital, and Baron Capital; specific percentages will be confirmed in the final beneficial ownership table. Aggregate insiders own more than 20% of Class A — material when read against the staged lockup. [CNN]

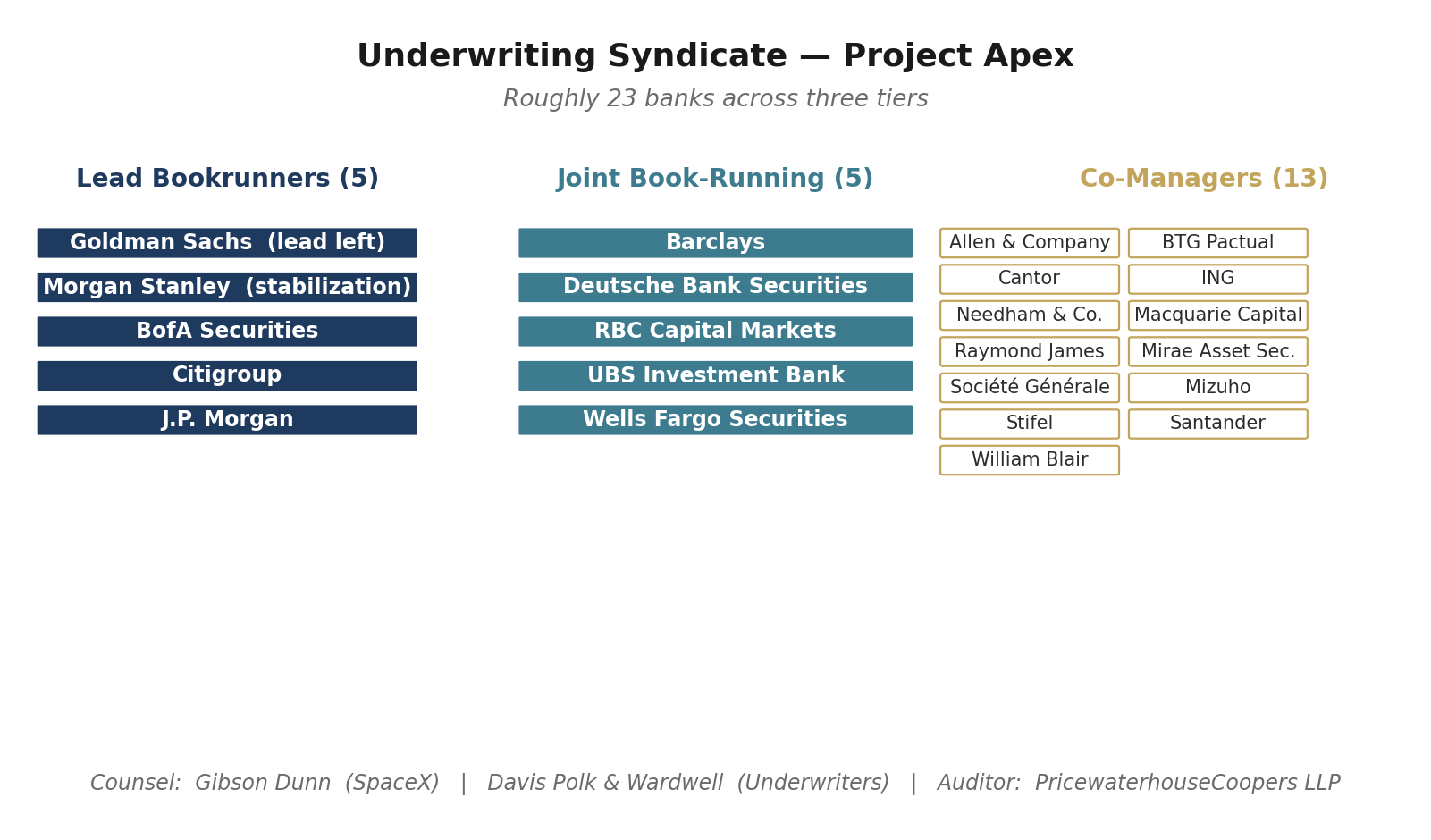

The deal, internally codenamed Project Apex, has five lead bookrunners plus 18 supporting banks (roughly 23 in total). Goldman Sachs holds the lead-left position; Morgan Stanley is the stabilization agent. The remaining lead bookrunners are BofA Securities, Citigroup, and J.P. Morgan. [AOL] [CNBC] [Texas Lawbook]

Figure 3. The Project Apex syndicate by tier.

Goldman's lead-left over Morgan Stanley surprised parts of the Street given Musk's long-standing Morgan Stanley relationship on Tesla and X. Morgan Stanley's stabilization-agent role and reported responsibility for the retail allocation channel reflect that relationship even though the top slot went elsewhere. The 23-bank syndicate is unusually large for a U.S. domestic listing and is consistent with a deal targeting both global institutional demand and up to 30% retail allocation through Robinhood, Fidelity, and Charles Schwab.

Gibson, Dunn & Crutcher LLP is company counsel; the team is led by capital markets partners George Sampas (New York) and Hillary Holmes, Harrison Tucker, and Atma Kabad (Houston). Gibson Dunn also advised on the $17 billion EchoStar spectrum acquisition (September 2025) and the February 2026 xAI merger. Davis Polk & Wardwell LLP represents the underwriters, led by Byron Rooney and Stephen Byeff (New York) and Alan Denenberg (California). PricewaterhouseCoopers LLP is the independent auditor and signed the Exhibit 23.1 consent covering the restated consolidated financials. [Bloomberg Law] [Texas Lawbook] [SEC]

The valuation debate is one of the widest of any recent listing. The disagreement is not whether SpaceX is remarkable — virtually every commentator concedes it — but whether $1.75T to $2T fairly reflects a company with a $4.94 billion GAAP net loss and a structurally unprofitable AI segment.

Four pillars: (1) Starlink is a recurring-revenue infrastructure business at 39% segment operating margins with subscriber and unit-economic momentum; ARK Invest's published model targets Starlink revenue exceeding $300 billion at full constellation maturity. (2) Commercial launch is structurally a near-monopoly with growing federal contract flow. (3) The Anthropic compute deal proves COLOSSUS and COLOSSUS II can be monetized as hyperscale data-center assets at roughly $15 billion of annual contracted revenue at full ramp. (4) Index inclusion under FTSE Russell fast-entry rules is expected to drive substantial passive demand soon after listing.

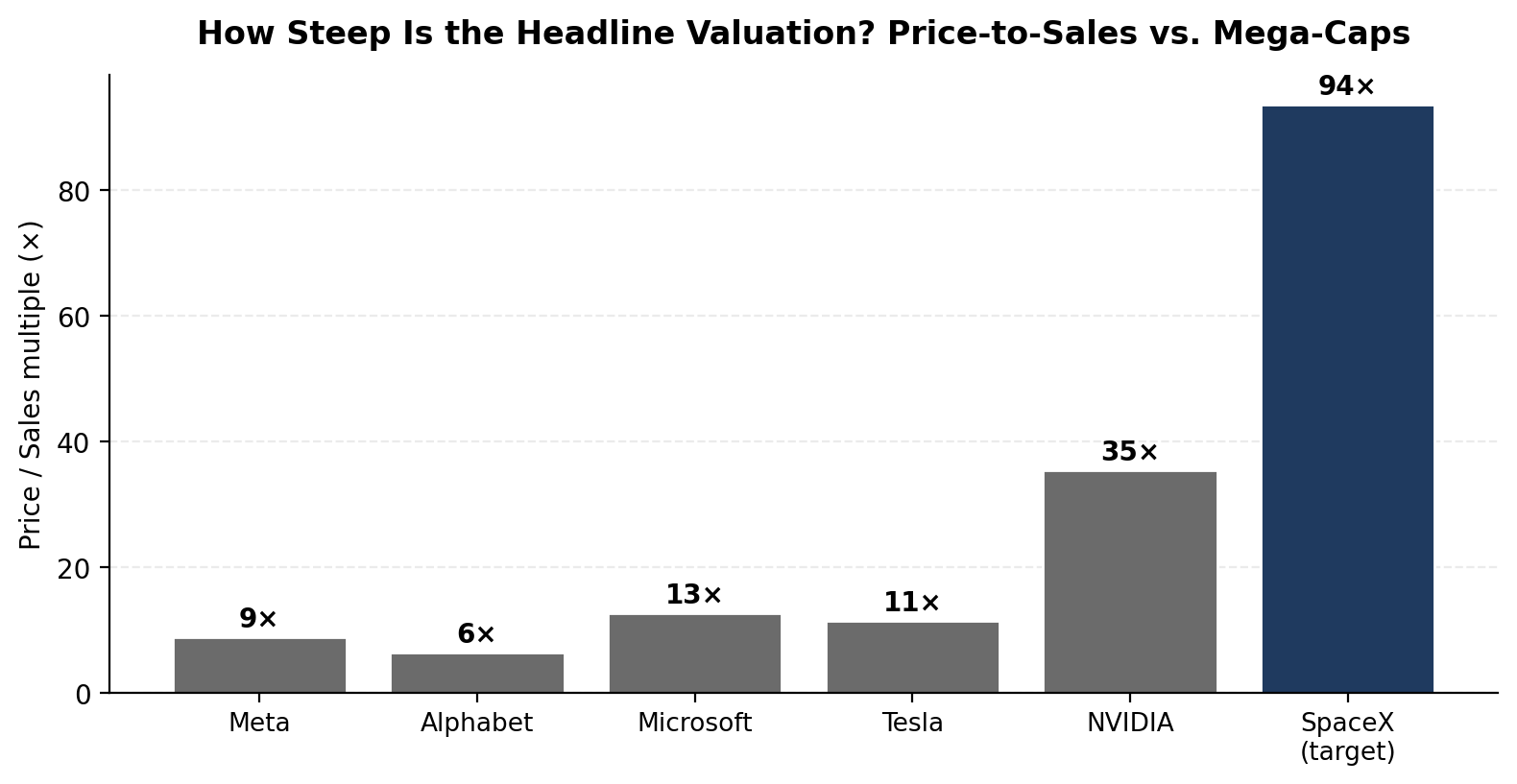

The starkest single number is the headline multiple: at $1.75T on $18.67B of revenue, SPCX would trade at roughly 94 times trailing sales — far above what the largest profitable U.S. tech companies trade at today.

Figure 4. SpaceX target P/S vs. large-cap tech. Indicative; rounded.

Other cautious points: public shareholders get economic exposure without practical voting leverage, the governance package is at the founder-protective extreme of the U.S. listing range, and the AI segment requires two future curves at once — durable hyperscale compute commitments longer than the 90-day Anthropic exit, and orbital data-center concepts that are referenced in the filing but not yet deployed. [Fortune]

Two items from filing week matter: SpaceX conducted Starship Flight 12 on May 21, and on May 27 the FAA ordered SpaceX to investigate a booster mishap from that flight. The anomaly does not affect Falcon 9 revenue, but it tempers any narrative that Starship is operationally routine. [Reuters]

Events worth tracking next:

• S-1 amendment with the initial price range at the start of the institutional roadshow in early June.

• Pricing in mid-June, with listing on Nasdaq and Nasdaq Texas under ticker SPCX.

• First quarterly earnings call as a public company (expected September 2026), which will determine whether the early-release lockup tier vests.

• Starship test cadence and any FAA findings from the Flight 12 booster investigation.

• Updates on the Anthropic compute relationship and whether either side exercises the 90-day termination right.

• Continued related-party and intercompany disclosures across SpaceX, xAI, X, and Tesla. [Reuters]

SEC EDGAR — SpaceX Form S-1 filing detail (May 20, 2026)

SEC — SpaceX S-1 main prospectus and exhibits (Exhibit 3.1 charter; Exhibit 5.1 Gibson Dunn legal opinion; Exhibit 23.1 PwC consent)

Reuters — "Bound for Mars: Elon Musk's SpaceX unveils filing for blockbuster IPO" (May 20, 2026)

Reuters — "Only Elon Musk can fire Elon Musk" (April 29, 2026); "SpaceX to allow early share resale" (May 22, 2026); "FAA orders SpaceX to investigate Starship booster mishap" (May 27, 2026)

Axios — "Anthropic is paying SpaceX $15 billion per year" (May 20, 2026); "SpaceX not the behemoth everyone thought" (May 21, 2026)

CNBC — "SpaceX lines up 21 banks for mega IPO, code-named Project Apex" (April 1, 2026)

Fortune — SpaceX governance and CalPERS / New York controllers' objections (May 22, 2026)

Bloomberg Law — "Gibson Dunn, Davis Polk Grab Roles in SpaceX's Largest-Ever IPO"; Texas Lawbook — "Gibson Dunn Guides SpaceX on Potential Record-Shattering IPO"

The Motley Fool — "Seven important things investors learned from SpaceX's S-1" (May 22, 2026); CNN Business — board composition coverage; Business Insider — Antonio Gracias / Valor analysis

Disclaimer

This article is prepared for informational purposes only and reflects publicly available information as of late May 2026. Financial figures are taken from the S-1 and from press parsing of the filing where indicated. Comparative price-to-sales multiples are illustrative. This piece does not constitute legal, tax, accounting, or investment advice. First Cover provides D&O insurance, EDGAR filing services, and shareholder meeting services to public-company clients; this content is not a recommendation to buy, sell, or hold any security.

The AI IPO Race: When Private Valuations Meet Public Scrutiny

The AI IPO Race: When Private Valuations Meet Public Scrutiny